Business Car Insurance Florida: Costs, Coverage, How To Save

Table of Contents

Business car insurance in Florida covers vehicles used for work, offering protection that personal auto policies don’t; like liability, vehicle damage, and employee use. Premiums average $260–$270 per month for a single vehicle, but costs vary widely by industry, location, and driving history.

To save, business owners can bundle policies, raise deductibles, and invest in safety features, while avoiding common pitfalls like lapsed coverage or missing hired/non-owned auto protection.

Running a business in Florida means adapting to risks: heat, hurricanes, and yeah, insurance. If you or your team drive for work, even just part-time, personal auto coverage probably isn’t enough. Hauling equipment, making deliveries, or letting employees use their own vehicles? That’s where business car insurance comes in.

Florida’s commercial auto rules aren’t just stricter. They’re more expensive. Laws are complex. Premiums are volatile. And the smallest oversight could leave your business exposed when you least expect it. But here’s the upside: once you understand how it works, what it costs, and what actually drives your rates, you can make smarter choices and potentially save thousands each year.

What you’ll find in this guide:

- The must‑know basics of business car insurance Florida requires

- What coverage really costs, and why it varies so much

- Proven ways to lower your premium without cutting corners

- A quick real-life case of how one Florida contractor saved 15%

What is commercial auto insurance?

Commercial auto insurance is designed for vehicles used on the job (not just for getting to and from work). Think delivery vans, work trucks, or even your own car if you’re running client errands or hauling gear during business hours.

It covers the kinds of risks personal auto insurance usually won’t touch once a vehicle crosses into business use. That includes:

- liability if your driver causes an accident

- damage to your business vehicle

- medical costs for injured passengers

- protection against uninsured or underinsured drivers

Basically, if a vehicle is tied to your business in any way (whether it’s owned, leased, or borrowed) you’ll want this coverage in place. Personal policies just aren’t built to handle business exposure, and relying on them could leave you unprotected when it matters most.

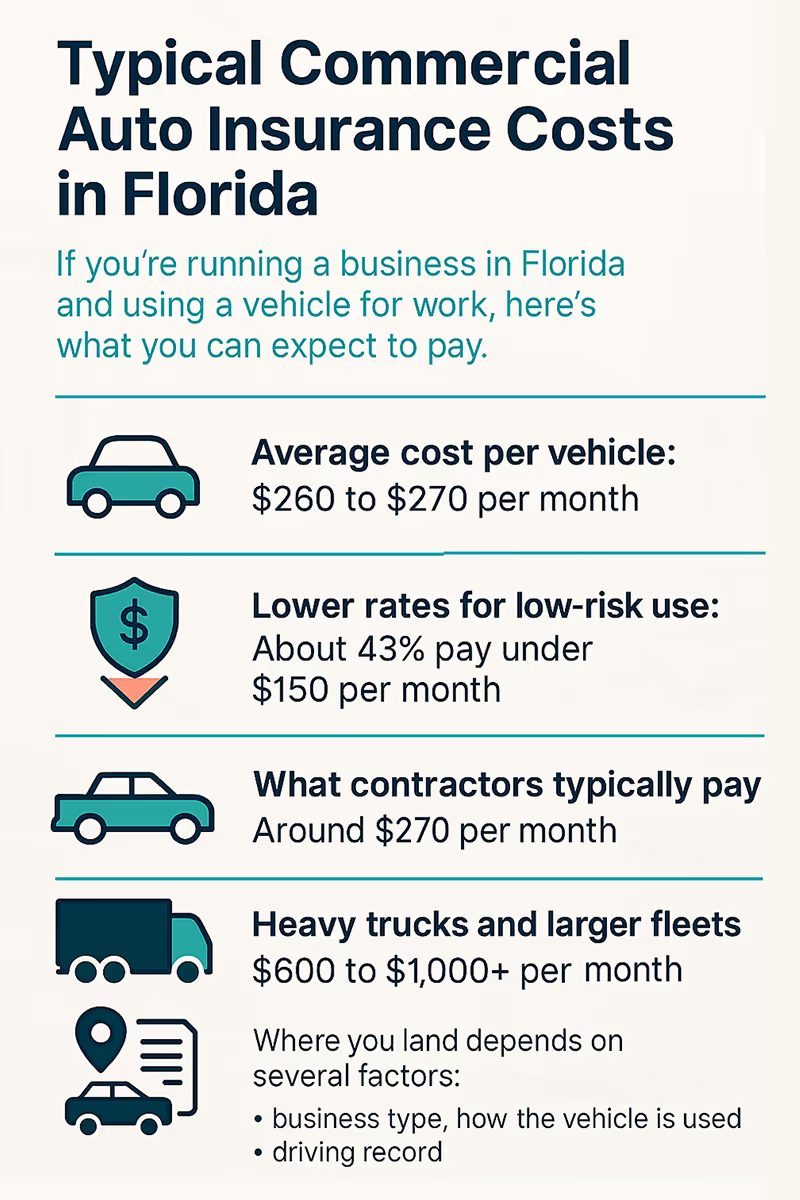

Typical commercial auto insurance costs in Florida

If you're running a business in Florida and using a vehicle for work, here's what you can expect to pay.

- Average cost per vehicle: Most Florida businesses pay around $260 to $270 per month, or roughly $3,200 per year. That’s the ballpark for a single vehicle with moderate use and clean driving history.

- Lower rates for low-risk use: About 43% of small businesses pay under $150 per month, especially if they operate just one or two vehicles and keep mileage low. So if you’re a solo operator or only use a car for occasional work errands, your premiums could fall on the lower end.

- What contractors typically pay: For trades like plumbing, HVAC, or electrical work (where pickup trucks or vans are used to haul tools and materials) monthly premiums tend to land around $270, right in line with the Florida average.

- Heavy trucks and larger fleets: If your business relies on freight transport, box trucks, or runs a small fleet, expect higher premiums, typically $600 to $1,000+ per vehicle per month. The added weight, distance, and exposure to road risk drive these costs up quickly.

- Where you land depends on several factors: Business type, how the vehicle is used, location, and driving record all come into play. For instance, operating in Miami or coastal areas (prone to hurricanes) often results in higher premiums. On the flip side, a safe driving history, fewer claims, and part-time vehicle use can help keep your costs on the lower side of the spectrum.

In short: there's no single price tag for business car insurance in Florida. But if you know where you fit, you can plan (and negotiate) smarter.

Why does Florida business car insurance cost more?

In short: Florida is one of the riskiest places in the country to insure a business vehicle. And that shows up in the premiums.

- High accident rates: Florida consistently ranks near the top for commercial vehicle crashes, especially in urban areas with heavy traffic and high delivery volumes.

- Lawsuits and inflated claims: Litigation plays a big role here. Some insurers report that over 70% of payout dollars go not to repair costs, but to attorneys and public adjusters. That kind of claims environment drives prices up across the board.

- Storm damage and weather volatility: Hurricanes and tropical storms aren’t just a headline issue. They show up in comprehensive claims. Businesses operating near the coast tend to face much higher premiums because of it.

- Even with reforms, prices are still rising: While state-level reforms have started to slow the pace, Florida’s business auto premiums are still increasing (about 10% annually through 2025), which is roughly double the national average.

So yes, there’s been progress. But the market’s still tough. Especially for small businesses trying to insure work vehicles without blowing up the budget.

What drives your business car insurance premium up or down

Your rate isn’t just pulled from thin air. It’s shaped by several factors. Some you can control. Others, not so much. Here's what insurers look at:

- Fleet size and usage: More vehicles on the road? More miles driven each month? That usually means more exposure to accidents, and higher premiums.

- Type of vehicle: Heavy-duty trucks, cargo vans, or anything carrying specialized equipment (like refrigeration units) tend to cost more to insure. They’re simply riskier to operate and more expensive to repair.

- Where you operate: If your business is based in high-traffic or high-risk areas: Miami-Dade, Fort Lauderdale, or coastal zones, expect your rates to reflect that. Urban congestion and storm exposure both push premiums up.

- Coverage limits and deductibles: Higher liability limits give you more protection, but they come at a cost. One way to balance that out is by raising your deductible. Just make sure you can cover it if something happens.

- Driver history and experience: Young, newly licensed, or accident-prone drivers are red flags for insurers. Clean records, on the other hand, can make a noticeable difference in your premium.

Bottom line: the more you reduce risk; whether that’s through better vehicles, better drivers, or smarter policy choices, the better your chances of lowering your rate.

How to reduce your business auto insurance premium

You might not control the weather or the roads. But there’s still a lot you can do to lower what you pay. Here’s where to start:

- Start shopping early. Don’t wait until your renewal notice shows up. Comparing quotes 90 to 120 days in advance gives you more leverage, and more time to make changes if needed.

- Bundle where it makes sense. If you also need general liability or a business owner’s policy (BOP), bundling with your commercial auto coverage can unlock meaningful discounts. Plus, it's simpler to manage.

- Adjust your deductibles wisely. Raising your deductible can shrink your monthly premium. But only do it if you’re financially comfortable covering those out-of-pocket costs if something goes wrong.

- Invest in safety and tracking. Using telematics (vehicle tracking), offering driver safety training, and keeping up with maintenance all help reduce perceived risk. Many insurers reward this with better pricing.

- Work with a broker. Florida’s market is... complicated. A good broker knows which insurers are writing business in your area and can help match you with carriers that understand your industry.

Every percentage point saved adds up, especially if you’re managing multiple vehicles or tight margins. The earlier you start, the more options you’ll have.

Common mistakes to avoid

Some insurance mistakes are small. Others can quietly unravel your whole policy when you least expect it. Here are a few to look out for:

- Listing the wrong location. If your vehicles operate in Florida but your paperwork says they’re based somewhere else (say, another state with cheaper rates) that’s a big red flag. Insurers consider it misrepresentation. At best, your claim gets denied. At worst, your entire policy could be voided. It’s not worth the risk.

- Letting coverage lapse, even briefly. You might think, "We’re not using the van right now. wWat’s the harm in pausing the policy?" But in Florida, even a short lapse can trigger a registration suspension. And once that happens, the reinstatement process isn't exactly quick or painless.

- Skipping hired/non-owned auto coverage. If an employee drives their own car for a quick delivery or to a job site, and they get into an accident? Your business could be held liable. Without this small but important coverage add-on, you’re wide open. And honestly, it’s one of those things most folks don’t realize they need until it’s too late.

These aren’t uncommon missteps. They happen when you’re busy, when you assume a personal policy will cover business use, or when you’re just trying to save money fast. But the consequences can be expensive and avoidable with a little foresight.

Key coverage options worth considering

State minimums might be legally enough. But they’re often nowhere near what your business actually needs. If you're serious about protecting your assets (and sleeping a little easier), here are some coverages worth adding to your policy:

- Bodily injury liability: aim for at least $250,000 per accident. Medical costs add up fast.

- Uninsured/underinsured motorist: in Florida, plenty of drivers don’t carry proper coverage. This protects you from their mistake.

- Collision and comprehensive: essential if you want coverage for storm damage, theft, or accidents where you're at fault.

- Cargo liability: especially if you're hauling tools, equipment, or goods for delivery.

- Hired/non‑owned auto (HNOA): for when employees drive their personal cars on the job. Easy to overlook, but hugely important.

- Cyber endorsements: more relevant now if you rely on GPS tracking, telematics, or vehicle-based data systems. A small add-on that covers a growing risk.

Many of these can be bundled with your general liability or folded into a business owner’s policy (BOP). Not only does that simplify coverage, it usually brings your total premium down, too.

It's one of those rare cases where better protection can actually cost less.

Ready to take next steps?

Florida’s commercial auto market is complex, but not inscrutable. By knowing the risks, choosing smart coverage levels, and shopping early, you can manage (even reduce) what you pay. When you're ready to see real options tailored to your business, use our free quote tool. You can test different scenarios; from single‑vehicle operations to multi‑truck fleets, and see how coverage settings shift costs.

Also, don’t forget to check our guides on general liability insurance and business owner’s policies to explore how bundling can bring cost savings without compromising coverage.

Florida business auto insurance costs more than average. But it doesn’t have to break your budget. With the right coverage, risk management, and shopping strategy, you can carry protection that works as smart as you do.

Frequently asked questions

Is personal auto insurance enough for business use?

No. Personal policies typically exclude business use, especially in Florida. If you're hauling tools, making deliveries, or using your vehicle for work tasks, personal coverage won’t respond, and that could leave you without protection in a crash.

What are Florida’s minimum coverage requirements for commercial vehicles?

Florida law requires at least $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL) for every registered vehicle (even commercial ones). That’s just the legal floor, not a recommended level for business operations.

How long will a claim impact your insurance rates?

Typically, a fault-based claim stays on your record for 2–3 years, but multiple claims or serious incidents can extend that period. Insurers track driving risk over longer spans, and premiums reflect that trend.

Should I compare multiple insurers or stick to one?

Definitely compare. Using an independent broker gives you access to multiple carriers, especially important in Florida’s volatile insurance landscape. It improves your chances of finding competitive pricing and better coverage alignment for your specific business type.

Can my personal vehicle be insured for business use under a commercial policy?

Yes, if it’s used for business purposes, many insurers will cover your personal vehicle under a commercial auto policy. Just be sure to declare the business use and ensure your industry and vehicle size meet the insurer’s criteria.

What if my employees use their own cars for work tasks?

You should definitely add a Hired and Non‑Owned Auto (HNOA) endorsement. Without it, any liability from employee-driven vehicles may fall back on your business. It’s often overlooked until a claim happens.

Driving in Florida comes with a specific set of legal requirements and coverage options, from personal injury protection to uninsured motorist coverage. Whether you're new to the state or just reviewing your current policy, our guide to Florida car insurance will help you make an informed decision.

Get a

Florida Home Insurance

Quote

To see how Worth can reduce your risk.